Week Ahead

Cooldown Before the Next Move? (Free Post)

Hello and welcome back to another SVC Update.

Looking back at the past week, we can confirm that the latest economic data has put some pressure on the recent strength of the US Dollar. While the releases only showed modest signs of renewed weakness, the key question going forward is whether this marks the beginning of a broader data trend. Until we see stronger confirmation, our core thesis remains unchanged.

Dollar Support Limited for the Time Being

This week’s US labor market report shifted some of the short-term risks, with the recent slowdown in US economic momentum appearing to maintain.

The US economy added 57K jobs in June 2026, well below the downwardly revised 129K recorded in May and below market expectations of 110K. It marked the weakest monthly job gain in four months, following three consecutive months of stronger-than-expected employment growth. Nevertheless, payroll growth remained broadly in line with the average monthly increase over the previous twelve months (+36K).

Employment continued to expand in professional and business services (+36K), social assistance (+25K), and healthcare (+22K). Meanwhile, leisure and hospitality lost 61K jobs, reflecting weaker-than-usual seasonal hiring, likely influenced by the FIFA World Cup. Employment remained largely unchanged across most other major industries, including construction, manufacturing, retail trade, transportation, financial activities, and government. In addition, payroll revisions reduced April and May employment by a combined 74K.

At the same time, the unemployment rate declined to 4.2% from 4.3%, coming in below expectations as labor force participation weakened. The number of unemployed individuals fell by 213K, while total employment declined by 507K. The labor force contracted by 720K, pushing the participation rate down to 61.5%, its lowest level since March 2021. The employment-population ratio also slipped to a four-year low of 59.0%, while the broader U-6 unemployment rate eased from 8.1% to 7.9%.

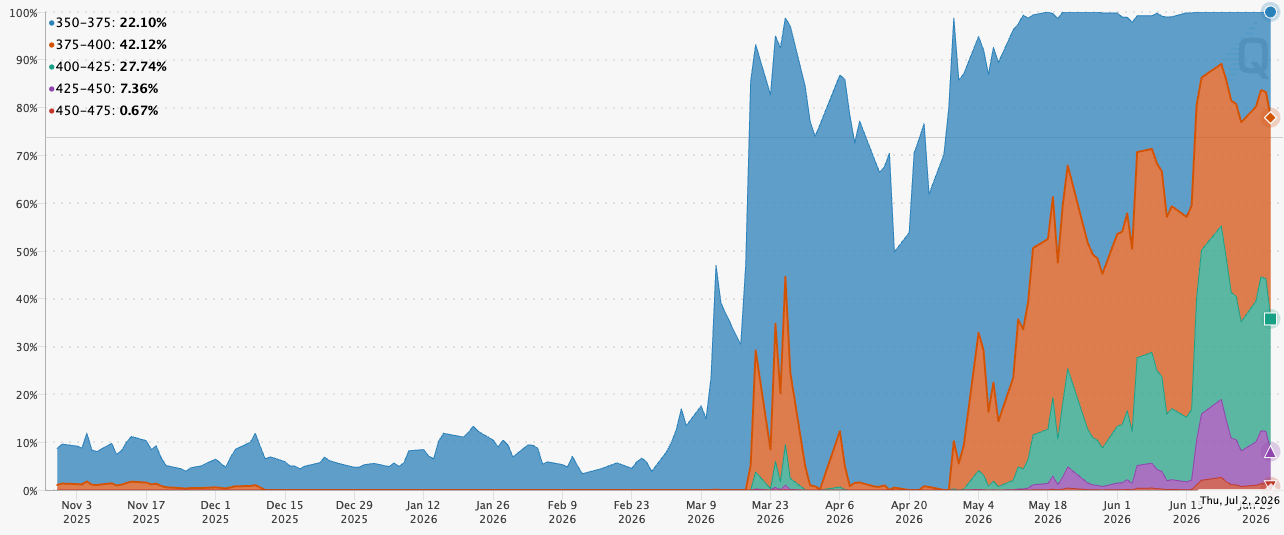

Current Fed Pricing

There are only limited event risks heading into next week, with attention already shifting towards July 14th, when US CPI inflation will be released alongside Fed Chair Warsh’s first semiannual testimony.

Without clear evidence of renewed disinflation, our broader Dollar bullish thesis remains intact. The recent pullback continues to provide attractive opportunities to build or add to existing Dollar long positions.

Upside Risk for the Yen

The combination of softer US data and a weaker Dollar has bought Japan’s Ministry of Finance additional time without the immediate need for another FX intervention.

We continue to expect the Bank of Japan to adopt a more hawkish stance over the coming months, with markets likely repricing the probability of a September rate hike, which is currently priced at only around 20%.

Japanese inflation is expected to remain elevated, requiring the BoJ to act more decisively in order to prevent another decline in real short-term interest rates.

Additional intervention risks could temporarily challenge our broader Dollar bullish view. However, this remains a market where relative strength versus weakness is critical. For that reason, we continue to avoid focusing on long USD/JPY exposure.

Recovery in Europe?

The Euro short has been one of the better-performing macro themes over recent months, primarily driven by relative economic data.

However, last week’s stronger Retail Sales and PMI releases provided renewed support for the Euro. Combined with the recent Dollar weakness, EUR/USD managed to establish a more solid near-term base.

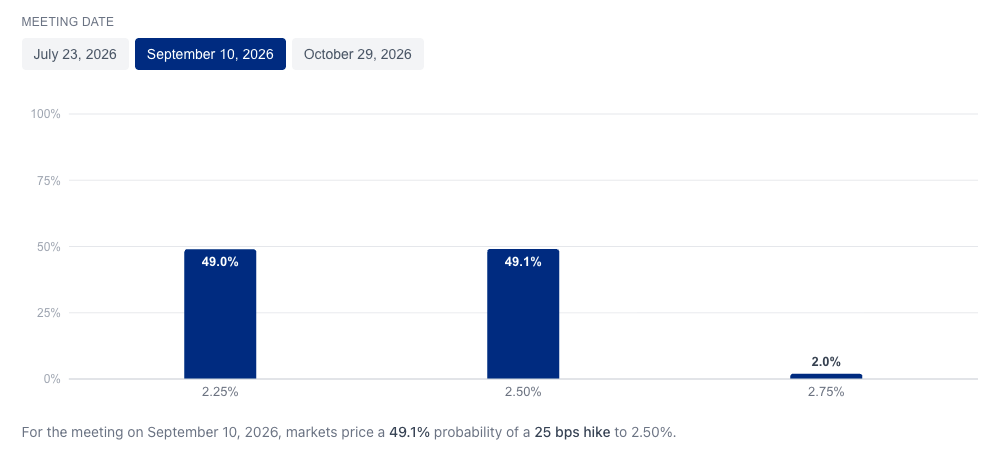

Looking ahead, next week’s inflation data will be particularly important. Should second-round inflation effects continue to push price pressures higher, it would strengthen the ECB’s credibility in delivering another rate hike, providing further support for the Euro. Current market pricing for both the ECB through September remains broadly balanced.

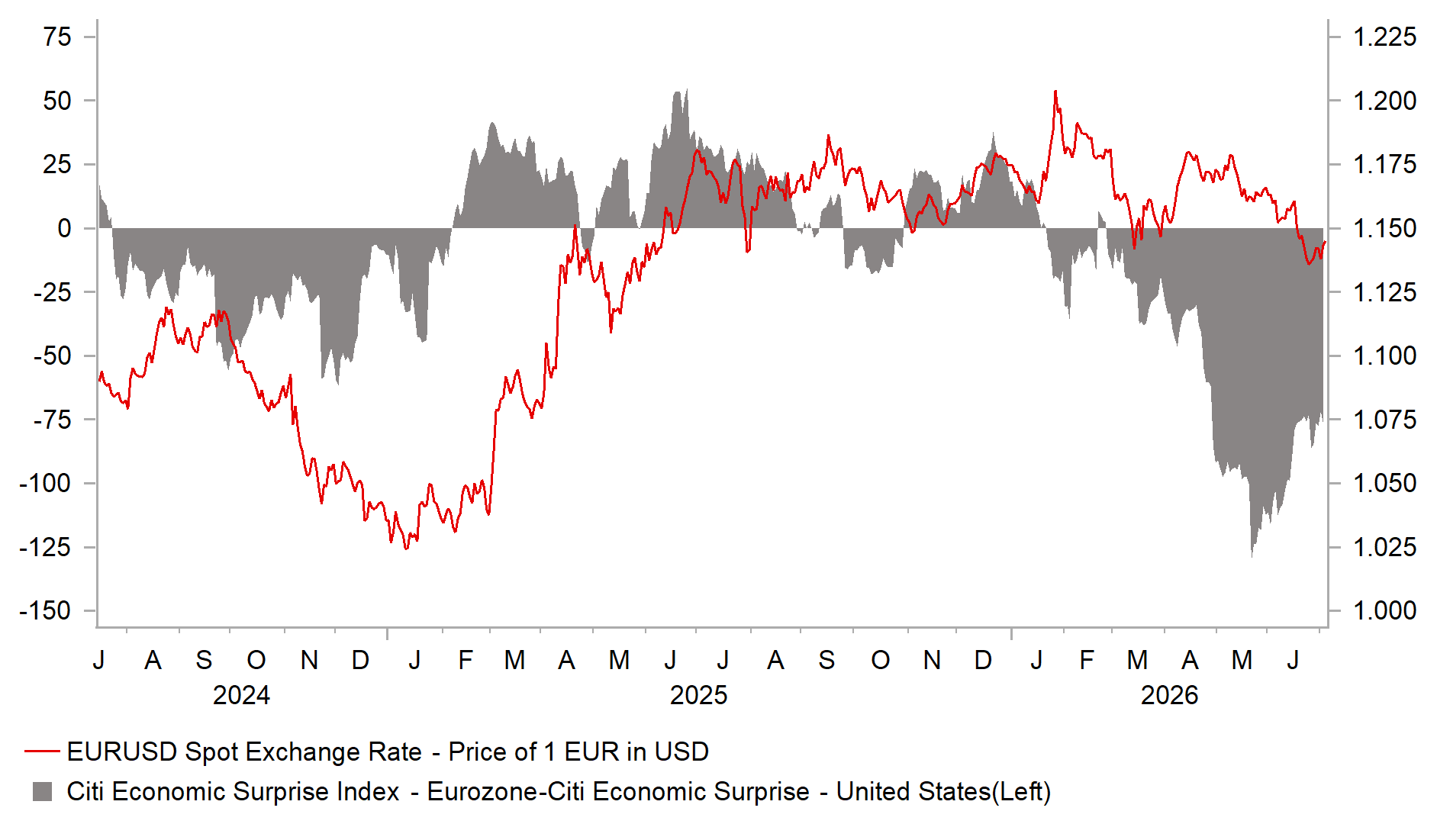

EUR/USD vs. Economic Surprise Index

While the Citi Economic Surprise Index (Eurozone relative to the US) has recently turned sharply negative, reflecting stronger-than-expected US economic surprises, EUR/USD has remained comparatively resilient.

This divergence suggests that FX markets are currently placing less emphasis on short-term macro surprises and are instead focusing more heavily on future interest rate expectations, yield differentials, and cross-border capital flows.

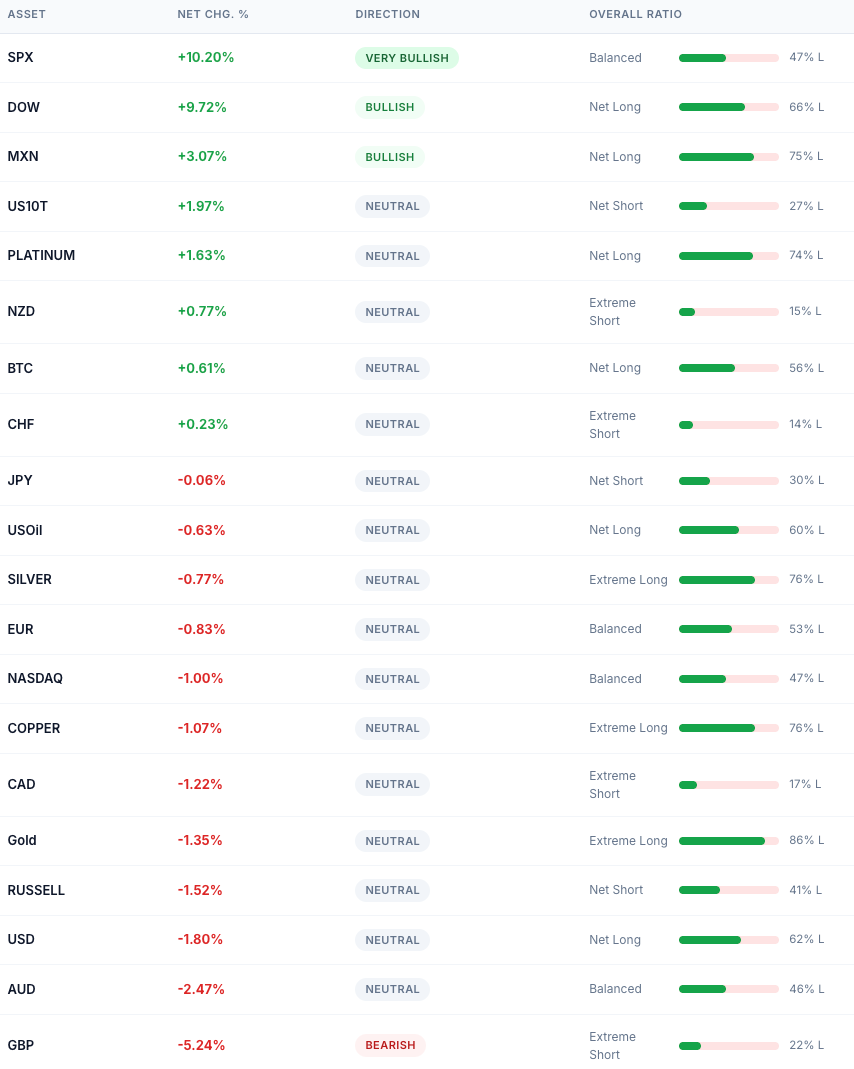

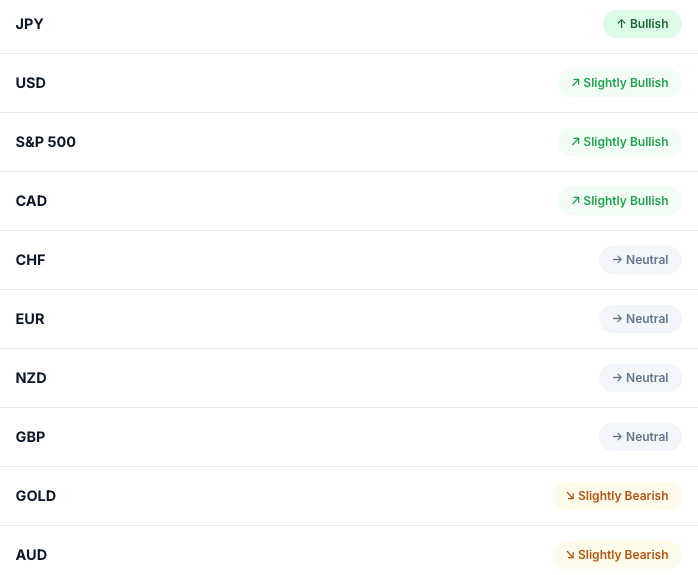

Institutional Positioning

Visualizer from the Gauch Research Terminal (Premium Access Only).

Outlook

Upcoming News

USD ISM Services PMI

NZD Cash Rate + RBNZ Statement / Press Conference

USD FOMC Meeting Minutes

EUR CPI

CAD UE Rate

Wishing you a successful week ahead,

David Gauch - Founder, Gauch Research

Similiar read on EURUSD here. The jobs print cooled the dollar off.

Watching the US 2-year now. If it stabilizes, the dollar probably holds together. If it keeps sliding, that stretched positioning may turn into a real problem

Thanks a lot for sharing your ideas!